PURPOSES

- To support the private sector to invest more in research and development of technology and innovation which will affect the economic development and elevate the national competitive competence

- To support and persuade the private sector to arrange research and development of technology and innovation for government and private agencies

300% TAX EXEMPTION INCENTIVE

A business operator can get 3 times tax exemption incentive from the actual expense on research and development of technology and innovation but not exceeding the maximum limit specified in percentage proportional to the revenue as follows:

- 6% of revenue for the amount exceeding 200 million Baht.

- 9% of revenue for the amount exceeding 20 million Baht but not exceeding 200 million Baht.

- 60% of revenue for the amount exceeding 50 million Baht.

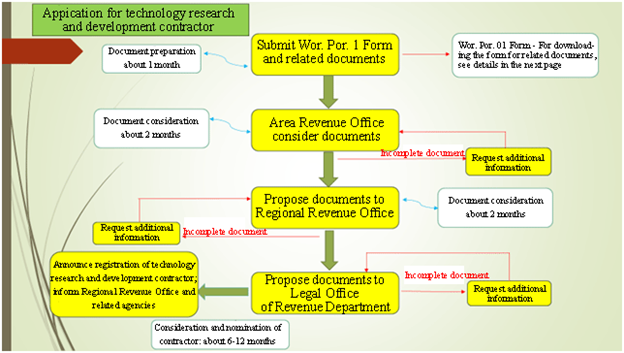

1.1 Process for submitting Wor. Por. 1 Form to the Revenue Department

SUPPORTING DOCUMENTS FOR APPLICATION FORM (WOR.PHOR. 01)

|

List |

Download Document |

|

1. Application Form of WOR.PHOR.01 |

|

|

2. Copy of establishment document showing the main objectives (in case of government agency, excluding ministry, bureau and department). |

|

|

3. Copy of company certificate issued by Registrar of Company Limited and Partnership Registration, memorandum of association and articles of associations (in case of juristic person). |

|

|

4. Copy of household registration and ID card (in case of natural person). |

|

|

5. List of researchers with Bachelor Degree and above in the field related to research and development of technology and innovation or equivalent, including detailed resume and copy of degree (separate full-time and part-time researchers). |

|

|

6. Copy of VAT registration (Phor.Phor. 20), if any. |

|

|

7. Copy of application of VAT registration (Phor.Phor. 01), if any. |

|

|

8. Copy of application for amendment of VAT registration (Phor.Phor. 09), if any. |

|

|

9. Example of receipt with the statement specified in Section 105 bis of Revenue Code including “A research and development grantee no. __________ of Announcement issued by Director General” and “Type of research: __________” |

|

|

10. List of machinery/equipment for research and development of technology and innovation, if any. |

|

|

11. Brief summary of current business operation. |

|

|

12. Plan for research and development of technology and innovation |

Contact Us:

The Revenue Department

RD Call Center 1161

TAX EXEMPTION INCENTIVE: Tel. 02-272-9056, 02-272-9822

1.2 NSTDA-Request for Research and Technology Development and Innovation (Wor Por 300%)

|

Contact for additional information Private Sector R&D Promotion Program Technology Management Center National Science and Technology Development Agency 111, Thailand Science Park, Phahonyothin Road, Khlong Nueng Subdistrct, Telephone: 0-2564-7000 – ext 1328 – 1332; and 1631 – 1634 http:// www.nstda.or.th/rdp |